- October 20, 2025

- Posted by: EWGFX

- Category: Technical analysis

The world’s financial architecture is being quietly rewritten. For decades, the U.S. dollar stood as the uncontested measure of global wealth — the universal language of central banks. But today, gold is beginning to speak louder.

Once dismissed as a relic of fallen empires, the “silent metal” has reclaimed its place in the modern reserve hierarchy. What began as a slow drift of confidence away from the dollar has become a migration of trust — and perhaps the start of a monetary regime shift.

Central banks, unsettled by sanctions, debt burdens, and the politicization of currencies, are restocking their vaults not for profit, but for protection. Each ton of bullion they add is not speculation — it’s a vote against vulnerability. And those votes are accumulating faster than almost anyone imagined.

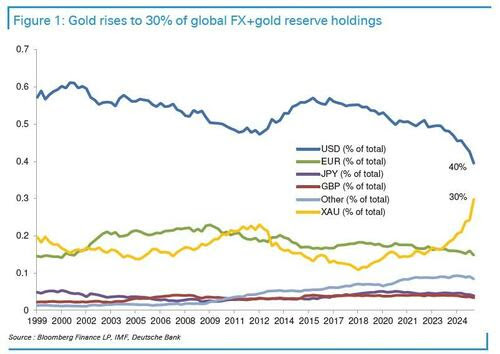

The numbers tell a story of transformation. Gold’s share of global FX reserves has risen from around 24% to nearly 30% in just months, while the dollar’s share has slipped toward 40%. That’s not a market fluctuation — it’s a tectonic realignment beneath the surface of global finance.

At the current pace, the crossover point — where gold overtakes the dollar as the world’s largest reserve asset — would occur around $5,800 per ounce.

According to Deutsche Bank, that’s roughly the “equilibrium” level where gold and the dollar would each account for about 36% of global reserves — a symbolic balance between the old world of credit and the new world of collateral.

But the deeper shift isn’t about valuation — it’s about validation. Gold has reasserted itself as the only asset without a counterparty — the ultimate “no one’s liability” instrument. In a system saturated with IOUs, that distinction now carries enormous weight.

The post–Bretton Woods era was built on credit and confidence. The post-Ukraine era appears to be rebuilding on custody and collateral. What looks like a rally in gold is, at its core, a repricing of sovereignty.

This isn’t a contest between metals and money — it’s a recalibration of what central banks consider real liquidity. Many observers mistake gold’s share of total central bank assets for its share of reserves, but those are very different universes.

Most central bank balance sheets are filled with domestic securities — euro paper for the ECB, Treasuries for the Fed — which reveal little about external firepower. The more meaningful measure is the ratio of gold to foreign-exchange reserves — the assets that can actually defend a currency.

Here, the data are striking. The ECB’s gold share of FX plus gold reserves was near 80% at the end of September (and about 83% if bullion is marked to $4,350/oz). Yet gold accounted for only 18% of its total balance sheet. The U.S. shows a similar split: roughly 96% of FX reserves but just 15% of total assets.

As Deutsche Bank notes, this growing gap explains why reserve managers increasingly benchmark against gold + FX reserves, rather than total assets. Those are the true war chest resources that can be mobilized in defense of a national currency — and gold’s relevance within that context is expanding every month.

Markets tend to lag such paradigm shifts. Traders chase stories; institutions chase safety. Eventually, the two converge — and when they do, the adjustment is rarely gentle.

A world where gold represents one-third of all official reserves isn’t one where the dollar collapses overnight — it’s one where confidence erodes slowly, then suddenly. Every ounce purchased by a reserve manager in Singapore or Riyadh, every basis point shaved from the U.S. share, forms part of a collective repositioning: out of promises, into proof.

We’re not just witnessing a bull market in gold — we’re witnessing a bear market in belief. The dollar’s supremacy was never about its paper or its color — it was about its credibility. Once that fades, the world reaches for something tangible — something it can hold.

Gold above $6,000 isn’t a fantasy number. It’s what happens when faith is repriced in ounces, not words.

The alchemists of the modern era aren’t turning lead into gold — they’re turning policy risk into metal. And as central banks continue voting with their balance sheets, they’re sending a message every trader already senses:

The true reserve asset of the future may not be a currency at all — but the oldest hedge in human history.