- January 19, 2026

- Posted by: EWGFX

- Category: Technical analysis

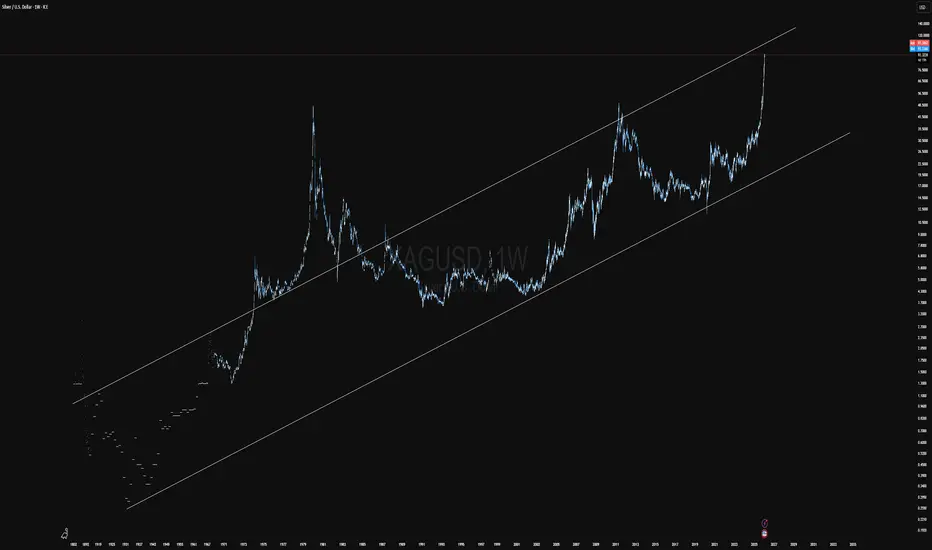

Long-horizon price behavior in Silver continues to exhibit persistent confinement within a statistically stable ascending channel, observable across multiple monetary regimes and volatility environments. This channel is not treated as a visual heuristic, but as an expression of long-run mean slope preservation, suggesting that Silver’s macro price evolution remains governed by slow-moving capital reallocation rather than episodic speculative dislocation.

Empirically, price action demonstrates repeated mean-reverting excursions around a rising central tendency, with volatility expanding near channel extremes and compressing near the midline. These dynamics are consistent with a bounded trend regime, wherein directional continuation is probabilistically favored following acceptance above the channel median, while terminal behavior is most frequently observed near the upper quantiles.

Historical expansion phases originating from the lower channel boundary have followed a similar path structure:

Prolonged accumulation within lower distribution percentiles

Acceptance above the channel midpoint

Convex acceleration toward the upper structural boundary

Liquidity exhaustion and multi-year corrective reversion

Crucially, prior encounters with the upper channel have not coincided with permanent trend failure, but with time-based redistribution phases that reset positioning before re-entering the primary regime. This reinforces the interpretation that Silver operates under cyclical volatility clustering rather than regime abandonment.

Of particular significance is the intertemporal stability of channel slope and amplitude. Despite heterogeneous macro inputs — including inflationary cycles, changes in real yield environments, and varying degrees of speculative leverage — the proportional geometry of price distribution remains invariant. From a quantitative standpoint, this implies that structural constraints dominate exogenous shocks, with price expressing shocks through range traversal rather than regime displacement.

At present, price exhibits sustained acceptance above the channel midpoint, a condition that historically increases the conditional probability of continuation toward upper-quartile valuations. However, from a risk-adjusted perspective, forward asymmetry diminishes as price approaches the upper boundary, where expected value shifts from directional continuation toward risk transfer and inventory offloading.

Until statistically significant acceptance occurs outside of the defined structural envelope, the null hypothesis remains intact:

Silver continues to operate within a mature ascending regime, characterized by rotational advances, volatility-mediated corrections, and long-duration equilibrium enforcement.

Structural deviation — not transient expansion — would be required to justify a regime reclassification.